Stack Sats or Stack Stablecoins ?

The second paradox of the synthetic-dollar race

🇬🇧 Read in English · 🇮🇹 Leggi in italiano

Stack Sats or Stack Stablecoins ?

The second paradox of the synthetic-dollar race

Federation Research — SATSINDEX Federation — May 2026

I. Two charts, one truth

We at the Federation read markets starting from charts, not from headlines. And right now there are two that, set side by side, tell the whole story.

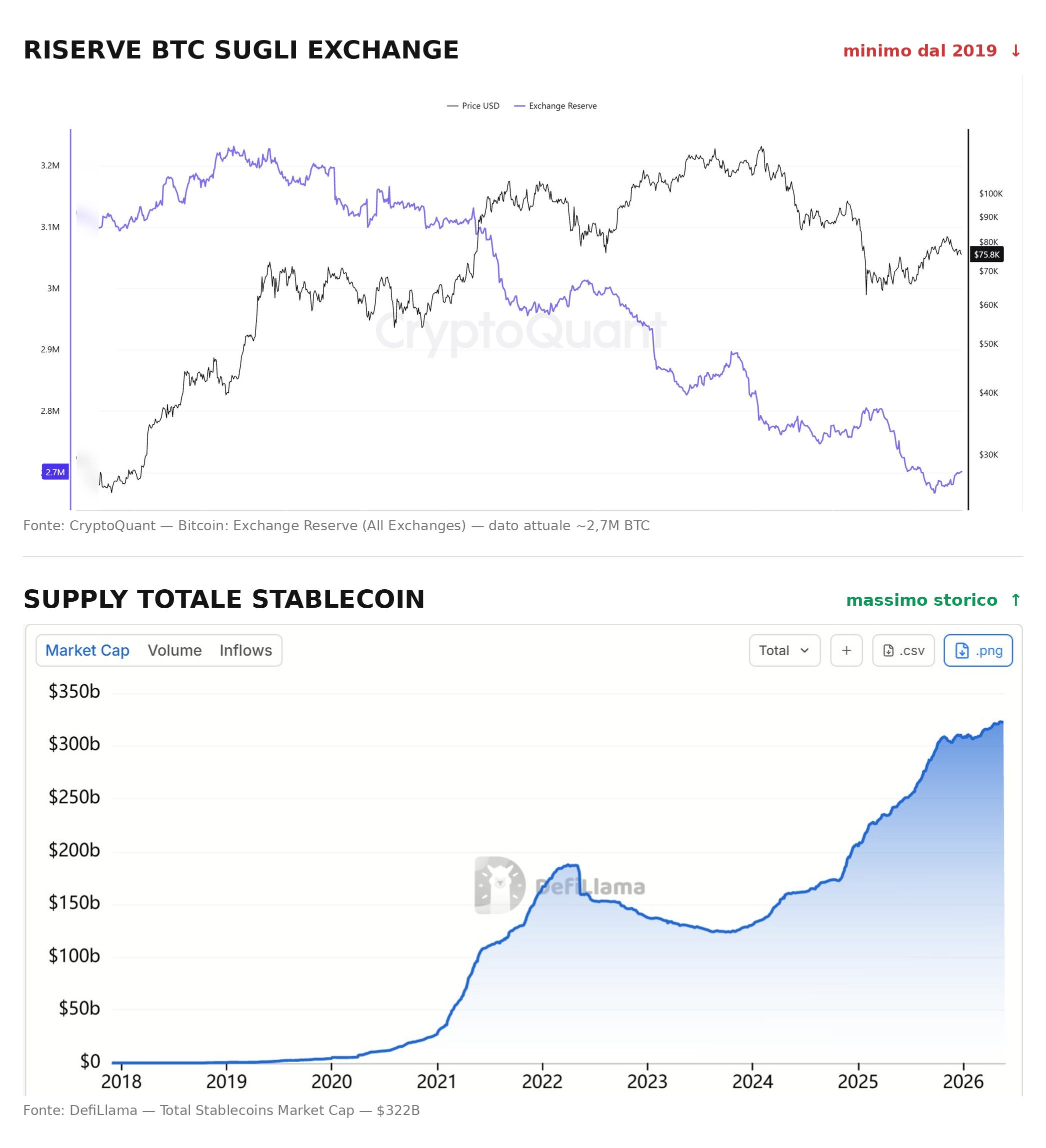

The first is falling. Bitcoin held on exchanges has dropped to roughly 2.7 million BTC — the lowest since 2019. Hundreds of thousands of coins have left the platforms over the past few years: withdrawn into self-custody, absorbed by funds, locked away in the vaults of those who have no intention of giving them back. This is not weakness. It is accumulation. It is the protocol’s scarcity doing its job.

The second is rising. The synthetic dollar-pegged currency has hit an all-time high, above 320 billion, and now moves 75% of all the trading volume in the crypto industry — the highest share ever recorded. When the market got scared, it did not take refuge in Bitcoin. It took refuge in the dollar. A dollar dressed up as a token, but a dollar all the same.

Here is the truth we read in the two charts together, and it is the thesis of this note: the asset everyone wants to own is being taken off the market and put away; the currency everyone wants to count in, trade in, exit into is still the dollar. Bitcoin has become the good to be held in custody. The dollar has remained the measure of everything. It is the exact opposite of the reason Bitcoin was born — and almost no one notices.

Then there is a third movement, quieter, that completes the picture.

In Trapani — famous, among other things, for the days of the mattanza of prized bluefin tuna — something used to happen that the rest of the world never saw. Japanese buyers would climb aboard the fishing boats during the customary passage of this renowned species and bargain over the tuna — a grade in high demand in Japan — while it was still underwater, not yet caught. Not a fish on the counter, not an auction at the harbor, but the promised catch, bought before it was even hauled up from the net. By the time the tuna reached shore, it already belonged to someone. The public market saw only the tail end of the story.

This is exactly what is happening to Bitcoin, and it is not a future scenario: it is already phase one. Miners no longer release their production drop by drop onto the exchanges where everyone can count it. They pool it and sell it in bulk on private desks; and upstream, on the hashrate markets, they sell forward the Bitcoin they have not yet mined — the tuna still underwater, not yet caught. On the other side, those who buy in volume don’t touch the public order books: they too go through OTC, so as not to move the price against themselves.

The paradox closes here. The metric retail watches with religious devotion — the Bitcoin flowing in and out of exchanges — is going blind precisely at the moment everyone is staring at it. By the time you see the coin appear on the visible market, someone will already have bought next year’s catch. And you will still be reading the tail end of the story.

II. The stolen numéraire

To understand how we got here, we have to remember what the dollar-pegged currencies were for, at the beginning. They were an emergency exit. A place to park value between one trade and the next, temporarily, while waiting to get back into the real asset. A technical convenience, not a destination.

That convenience took the whole pie. Today the synthetic currency is no longer the parking lot: it is the road. It has become the market’s unit of account, the measure by which everything is priced, traded and — above all — measured. About 99% of this mass is denominated in dollars. The volume it moves has surpassed that of the major traditional payment networks combined. It is no longer an emergency exit. It is the floor the entire ecosystem walks on.

And here the semantic deception kicks in, the one almost no one notices. Bitcoin was born as an escape route from fiat money — from a currency that whoever issues it can expand at will, and that by design loses purchasing power over time. The crypto space promised to give us a different measure. Instead it rebuilt the old measure inside itself, in synthetic form, and elected it as the default. We changed the track but not the destination station: it is still the dollar.

The numéraire — the unit in which a human being thinks wealth — is the hardest thing to move. Harder than price, harder than technology. And the market tells us so without shame: when fear arrives, the crowd does not run toward sats. It runs toward the disguised dollar. It does so even in the middle of a decline, rotating within the assets pegged to the greenback instead of leaving the ecosystem. Translated: it prefers to stay in crypto, but in its version that most resembles the very thing it claimed to be fleeing.

This is the stolen numéraire. It was not taken from us by force. We let it be taken back, one comfortable trade at a time.

III. The extinct niche

There is structural proof of all this, and it sits in a corner of the market the general public never looks at: the contracts.

There are two ways to trade a perpetual. One is margined in stablecoin — you post synthetic dollars as collateral, and your profits and losses are counted in dollars. The other is margined in the currency itself: you post Bitcoin as collateral, and everything — margin, profit, loss — is denominated in Bitcoin. The first is called linear. The second, inverse.

The first won across the board. And not by chance. It won for the same reason as everything else: because for most people the measure is the dollar, and counting in dollars is simple, while the math of the inverse — where the value of your position moves non-linearly relative to price — has to be explained. The market chose convenience, and convenience speaks dollar.

The result is that today, on decentralized platforms, trading Bitcoin denominated in Bitcoin is almost impossible. The major venues are all margined in synthetic dollars. The inverse survives as a niche on a few centralized exchanges, a reservation for the coin-margined, while all the volume and all the liquidity have moved elsewhere.

And so the question we ask is simple: where are the exchanges and the protocols that could have made this niche their bedrock? Where are the venues that put Bitcoin at the center not only as an asset to be priced, but as the unit in which to operate? They barely exist anymore, or they were never born. The market had the chance to build a natively Bitcoin infrastructure and chose, once again, the dollar.

This is not a technical detail for insiders. It is the stolen numéraire materializing in the code. When even the instrument for trading, investing and accumulating Bitcoin forces you to think in dollars, the circle has closed.

IV. The profit you don’t see

And yet that very abandoned niche holds the most powerful logic for anyone who truly believes in Bitcoin.

Trading inverse perpetuals — margined in BTC — is, and always has been, an excellent path to accumulation. A disciplined trader opens the setup, exits at a profit, and at that point takes at least 50% off the table, sends it to their own self-custody, and only then goes back to hunting for the next high-probability entry. Nothing esoteric: it is risk management applied with method. At the Federation we are advocates of technical analysis before narrative — show me the chart, I will tell you the news — in an age when a single social-media post seems to move the price more than a quarter of fundamentals.

Here someone will object: but I get the exact same result margined in stablecoin. I exit the profitable trade, scale the capital by 50%, buy Bitcoin and send it to self-custody. True in theory. The deception is in the practice, and it is twofold.

The first layer is mechanical: the double fee. You sell in dollars, you rebuy Bitcoin — two operations, two commissions, two spreads, every time.

The second layer is behavioral, and it is the one that matters. 90% of traders never convert that dollar value into Bitcoin. They are far more incentivized to re-enter the market with the whole sum — because, let us remember, that sum remains only a number on a screen — and in most cases they put it back on the table, undoing the profitable trade from before. The step “convert the profit into Bitcoin and withdraw it” is a friction that, left to voluntary discipline, almost no one performs. In Bitcoin margin that step does not exist: the profit is already in the right currency. The discipline is written into the vehicle, not entrusted to willpower.

And here is the inversion the market does not see. The profit in dollars seems the certain, real, accountable value. The profit in Bitcoin seems negligible — a number with too many zeros in front of it. But it is exactly the opposite. The dollar is the apparently certain, destined to lose purchasing power by design of the system that issues it. That small number of Bitcoin is the apparently negligible that, by the scarcity written into the protocol, becomes the real value over time. The sats accumulated in 2018 prove it today, with no need for further argument: the sum that seemed like nothing back then tells a different story now.

One truth remains that we do not hide, because those who do research do not shill: all of this holds on the accumulation vector, not on the risk vector. Leverage cuts both ways. A liquidation does not just force you out of a trade — it destroys the very stack you were building, and the scarcity written into the protocol does not compensate a liquidated position. Bitcoin margin is an excellent instrument for those who know how to manage risk and have discipline — a word too often underrated. It is not a magic button, and we are not selling it to you as one.

V. The retail trap

So the question becomes inevitable: why does 90% of traders accumulate synthetic currency — stablecoins — instead of Lord Sats?

The answer is uncomfortable, because it is not stupidity. It is incentive. Pulling dollars is simpler to account for, more straightforward to declare to the taxman, more convenient to keep on the books without the volatility that turns your stomach. And above all there is the dopamine: the number go up the brain chases is measured in dollars. Watching the balance grow in synthetic currency gives an immediate satisfaction that the small number of Bitcoin, with its zeros, cannot. This perspective can be flipped — not by changing Bitcoin, which is already what is needed, but by changing the measure. Learning to count in sats what we count today in dollars is not a technical dream: it is a choice that can be made workable. The instruments to count, trade and read the world in sats can be built. Sooner or later someone will build them.

The cost, though, is hidden — and that is exactly the trap. Whoever accumulates synthetic currency measures their financial life in the unit they were fleeing from. They feel safe in the asset designed, by construction, to lose purchasing power. The sense of safety is real; the safety is not. It is the comfort of staying on the known shore while the tide, slowly, raises the level of the water.

And there is one last layer, which closes the circle opened in the first section. While retail pulls synthetic dollars, institutions pull Bitcoin at a speed the miners cannot satisfy. Institutional demand now absorbs more than the new currency the miners put out — recently about double. Miners generate roughly 450 BTC a day; the listed vehicles alone, according to Bitwise, risk absorbing more than 100% of the entire year’s issuance over the course of 2026 — a supply-demand dynamic with no precedent in the asset’s history. On one side, those who own the asset take it off the market and keep it. On the other, those who should own it accumulate promises of dollars.

There is no need to add anything else. The two behaviors, set side by side, are the real chart of this note.

VI. Give Bitcoin back to the people

It makes you wonder, then, where the promise went. Financial freedom, self-sovereignty, the old HODL, the cypherpunk ethic from which all this started. Were they corrupted?

Our answer is no. They were not corrupted. They were made inconvenient.

The principles were not touched in the code. The protocol is exactly what it has always been: the scarcity is there, self-custody works, no one has dismantled it — on the contrary, it is more widespread today than ever. And it has a precise birth date: in November 2022, in the month a major exchange collapsed, over 325,000 BTC left the platforms in a matter of weeks. It was fear that taught people to hold their own coins. Since then the movement has never stopped — and it is exactly why exchange reserves keep falling. What changed is not the possibility. It is the default. Once, sovereignty was the only road available. Today it is one of two, and it is the harder one: the one you have to choose with intention, against the current of convenience that pushes you toward the synthetic dollar at every step.

This is the real battlefield. Not between Bitcoin and the banks. Between convenience and intention. The swindle underway is not a conspiracy: it is a drift, a thousand small comfortable choices that, summed up, hand the numéraire back to the very fiat system Bitcoin was born to surpass.

That is why we say it plainly, and we say it to those who read us even before we say it to the markets: give Bitcoin back to the people. Give Bitcoin back to the people — and give it back in the only form that counts, the one in which Bitcoin is the measure, not the object to be priced in dollars. Go back to counting in sats. Go back to taking off the table and holding in custody. Go back to reading the chart instead of the post.

Inconvenience is not a sentence. It is a choice. And every stack of sats, today, is that choice made concrete.

The Federation is a collective of independent Bitcoin researchers and builders. I speak on its behalf. We don’t disclose membership — the work speaks for itself.

Accumulare sats o accumulare stablecoin?

Il secondo paradosso della corsa al dollaro sintetico

Federation Research — SATSINDEX Federation — Maggio 2026

I. Due grafici, una verità

Noi della Federation guardiamo i mercati partendo dai grafici, non dai titoli. E in questo momento ce ne sono due che, messi vicini, raccontano tutto.

Il primo scende. I Bitcoin custoditi sugli exchange sono scesi a circa 2,7 milioni di BTC — il minimo dal 2019. Centinaia di migliaia di monete hanno lasciato le piattaforme negli ultimi anni: ritirate in autocustodia, assorbite dai fondi, chiuse in caveau di chi non ha intenzione di restituirle. Non è debolezza. È accumulo. È la scarsità del protocollo che fa il proprio lavoro.

Il secondo sale. La moneta sintetica agganciata al dollaro ha toccato il massimo storico, oltre 320 miliardi, e muove ormai il 75% di tutto il volume di scambio dell’industria crypto — la quota più alta mai registrata. Quando il mercato ha avuto paura, non si è rifugiato in Bitcoin. Si è rifugiato nel dollaro. Un dollaro travestito da token, ma sempre dollaro.

Qui sta la verità che leggiamo nei due grafici insieme, ed è la tesi di questa nota: l’asset che tutti vogliono possedere viene tolto dal mercato e messo via; la valuta in cui tutti vogliono contare, scambiare, uscire resta il dollaro. Bitcoin è diventato il bene da custodire. Il dollaro è rimasto il metro di ogni cosa. È l’esatto opposto del motivo per cui Bitcoin è nato — e quasi nessuno se ne accorge.

C’è poi un terzo movimento, più silenzioso, che chiude il quadro.

A Trapani, famosa anche per i giorni della mattanza del pregiato tonno rosso, succedeva una cosa che il resto del mondo non vedeva. I compratori giapponesi salivano a bordo dei pescherecci nei canonici periodi di passaggio di questa rinomata specie e contrattavano il tonno — una qualità richiestissima in Giappone — quando era ancora sott’acqua, non ancora pescato. Non un pesce sul bancone, non un’asta al porto, ma la cattura promessa, comprata prima ancora di essere tirata su dalla rete. Quando il tonno arrivava a riva, era già di qualcuno. Il mercato pubblico vedeva solo la coda della storia.

È esattamente ciò che sta accadendo a Bitcoin, e non è uno scenario futuro: è già la fase uno. I miner non versano più la loro produzione goccia a goccia sugli exchange dove tutti la possono contare. La accorpano e la vendono in blocco su desk privati; e a monte, sui mercati hashrate, vendono in avanti il Bitcoin che ancora non hanno minato — il tonno ancora sott’acqua, non ancora pescato. Dall’altro lato, chi compra in volume non tocca i book pubblici: passa anch’esso dall’OTC, per non muovere il prezzo contro sé stesso.

Il paradosso si chiude qui. La metrica che il retail osserva con religione — i Bitcoin che entrano ed escono dagli exchange — sta diventando cieca proprio nel momento in cui tutti la fissano. Quando vedrai la moneta comparire sul mercato visibile, qualcuno avrà già comprato la pesca dell’anno prossimo. E tu starai ancora leggendo la coda della storia.

II. Il numéraire rubato

Per capire come ci siamo arrivati bisogna ricordare a cosa servivano, all’inizio, le valute agganciate al dollaro. Erano un’uscita di sicurezza. Un posto dove parcheggiare valore tra un’operazione e l’altra, temporaneamente, in attesa di rientrare nell’asset vero. Una comodità tecnica, non una destinazione.

Quella comodità si è presa tutta la torta. Oggi la moneta sintetica non è più il parcheggio: è la strada. È diventata l’unità di conto del mercato, il metro con cui tutto viene prezzato, scambiato e — soprattutto — misurato. Circa il 99% di questa massa è denominata in dollari. Il volume che muove ha superato quello dei grandi circuiti di pagamento tradizionali messi insieme. Non è più un’uscita di sicurezza. È il pavimento su cui cammina l’intero ecosistema.

E qui scatta l’inganno semantico che quasi nessuno nota. Bitcoin nasce come via di fuga dal denaro fiat — da una moneta che chi la emette può espandere a piacimento, e che per disegno perde potere d’acquisto nel tempo. Lo spazio crypto prometteva di darci un metro diverso. Invece ha ricostruito il vecchio metro al proprio interno, in forma sintetica, e lo ha eletto a default. Abbiamo cambiato il binario ma non la stazione di arrivo: è ancora il dollaro.

Il numéraire — l’unità in cui un essere umano pensa la ricchezza — è la cosa più difficile da spostare. Più del prezzo, più della tecnologia. E il mercato ce lo dice senza pudore: quando arriva la paura, la massa non corre verso i sats. Corre verso il dollaro travestito. Lo fa anche nel pieno di una discesa, ruotando dentro gli asset agganciati al biglietto verde invece di uscire dall’ecosistema. Tradotto: preferisce restare in crypto, ma nella sua versione che assomiglia di più a ciò da cui dichiarava di fuggire.

Questo è il numéraire rubato. Non ce l’hanno tolto con la forza. Ce lo siamo fatti riprendere, un trade comodo alla volta.

III. La nicchia estinta

C’è una prova strutturale di tutto questo, e sta in un angolo del mercato che il grande pubblico non guarda mai: i contratti.

Esistono due modi di tradare un perpetual. Uno è a margine in stablecoin — metti dollari sintetici come collaterale, e profitti e perdite te li conta in dollari. L’altro è a margine nella moneta stessa: metti Bitcoin come collaterale, e tutto — margine, profitto, perdita — è denominato in Bitcoin. Il primo si chiama lineare. Il secondo, inverse.

Il primo ha vinto su tutta la linea. E non per caso. Ha vinto per la stessa ragione di tutto il resto: perché per la maggior parte delle persone il metro è il dollaro, e contare in dollari è semplice, mentre la matematica dell’inverse — dove il valore della tua posizione si muove in modo non lineare rispetto al prezzo — va spiegata. Il mercato ha scelto la comodità, e la comodità parla dollaro.

Il risultato è che oggi, sulle piattaforme decentralizzate, tradare Bitcoin denominato in Bitcoin è quasi impossibile. I principali venue sono tutti a margine in dollari sintetici. L’inverse sopravvive come nicchia su qualche exchange centralizzato, una riserva indiana del coin-margined, mentre tutto il volume e tutta la liquidità si sono spostati altrove.

E allora la domanda che poniamo è semplice: dove sono finiti gli exchange e i protocolli che di questa nicchia avrebbero potuto fare il proprio zoccolo duro? Dove sono i venue che mettono Bitcoin al centro non solo come asset da prezzare, ma come unità in cui operare? Non esistono quasi più, o non sono mai nati. Il mercato ha avuto la possibilità di costruire un’infrastruttura nativamente Bitcoin e ha scelto, di nuovo, il dollaro.

Non è un dettaglio tecnico per addetti ai lavori. È il numéraire rubato che si materializza nel codice. Quando perfino lo strumento per tradare, investire e accumulare Bitcoin ti obbliga a pensare in dollari, il cerchio si è chiuso.

IV. Il profitto che non vedi

Eppure proprio quella nicchia abbandonata custodisce la logica più potente per chi crede davvero in Bitcoin.

Tradare inverse perpetual — a margine in BTC — è, ed è sempre stata, un’ottima via di accumulo. Un trader disciplinato apre il setup, esce a profitto, e a quel punto leva dal tavolo almeno il 50%, lo manda nella propria self-custody, e solo allora torna a cercare il prossimo ingresso ad alta probabilità di profitto. Niente di esoterico: è gestione del rischio applicata con metodo. Alla Federation siamo sostenitori dell’analisi tecnica prima della narrativa — show me the chart, I will tell you the news — in un’epoca in cui un singolo post su un social sembra muovere il prezzo più di un trimestre di fondamentali.

Qui qualcuno obietterà: ma lo stesso identico risultato lo ottengo a margine in stablecoin. Esco dal trade profittevole, scalo il capitale del 50%, compro Bitcoin e lo mando in self-custody. Vero in teoria. L’inganno è nella pratica, ed è doppio.

Il primo strato è meccanico: la doppia fee. Vendi in dollari, ricompri Bitcoin — due operazioni, due commissioni, due spread, ogni volta.

Il secondo strato è comportamentale, ed è quello che conta. Il 90% dei trader non monetizza mai quel valore in dollari verso Bitcoin. È molto più incentivato a rientrare a mercato con l’intera somma — perché, ricordiamolo, quella somma resta soltanto un numero su uno schermo — e nella maggior parte dei casi la rilascia di nuovo sul tavolo, vanificando il trade profittevole di prima. Il passaggio “converti il profitto in Bitcoin e ritiralo” è un attrito che, lasciato alla disciplina volontaria, quasi nessuno compie. Nel margine in Bitcoin quel passaggio non esiste: il profitto è già nella moneta giusta. La disciplina è scritta nel veicolo, non affidata alla forza di volontà.

E qui sta l’inversione che il mercato non vede. Il profitto in dollari sembra il valore certo, reale, contabilizzabile. Il profitto in Bitcoin sembra irrisorio — un numero con troppi zeri davanti. Ma è esattamente il contrario. Il dollaro è l’apparente certo, destinato a perdere potere d’acquisto per disegno del sistema che lo emette. Quel numero piccolo di Bitcoin è l’apparente irrisorio che, per la scarsità scritta nel protocollo, nel tempo diventa il vero valore. I sat accumulati nel 2018 lo dimostrano oggi, senza bisogno di altri argomenti: la somma che allora sembrava nulla, oggi racconta un’altra storia.

Resta una verità che non nascondiamo, perché chi fa ricerca non shilla: tutto questo vale sul vettore di accumulo, non sul vettore di rischio. La leva taglia in due sensi. Una liquidazione non ti fa solo uscire forzatamente da un trade — ti distrugge proprio lo stack che stavi costruendo, e la scarsità scritta nel protocollo non risarcisce una posizione liquidata. Il margine in Bitcoin è uno strumento eccellente per chi sa gestire il rischio e ha disciplina — un vocabolo troppo spesso sottovalutato. Non è un pulsante magico, e noi non te lo vendiamo come tale.

V. La trappola del retail

Allora la domanda diventa inevitabile: perché il 90% dei trader accumula moneta sintetica — stablecoin — invece di Lord Sats?

La risposta è scomoda, perché non è stupidità. È incentivo. Staccare dollari è più semplice da contabilizzare, più lineare da dichiarare al fisco, più comodo da tenere a bilancio senza la volatilità che fa venire il mal di stomaco. E soprattutto c’è la dopamina: il number go up che il cervello insegue è misurato in dollari. Vedere il saldo crescere in valuta sintetica dà una soddisfazione immediata che il piccolo numero di Bitcoin, con i suoi zeri, non riesce a dare. Questa prospettiva si può ribaltare — non cambiando Bitcoin, che è già quello che serve, ma cambiando il metro. Imparare a misurare in sats ciò che oggi misuriamo in dollari non è un sogno tecnico: è una scelta che si può rendere praticabile. Gli strumenti per contare, scambiare e leggere il mondo in sats si possono costruire. Prima o poi qualcuno li costruirà.

Il costo, però, è nascosto — ed è esattamente la trappola. Chi accumula moneta sintetica misura la propria vita finanziaria nell’unità da cui stava fuggendo. Si sente al sicuro nell’asset progettato, per costruzione, per perdere potere d’acquisto. Il senso di sicurezza è reale; la sicurezza non lo è. È il comfort di restare sulla riva conosciuta mentre la marea, lentamente, alza il livello dell’acqua.

E c’è un ultimo strato, che chiude il cerchio aperto nella prima sezione. Mentre il retail stacca dollari sintetici, le istituzioni staccano Bitcoin a una velocità che i miner non riescono a soddisfare. La domanda istituzionale assorbe ormai più della nuova moneta che i miner immettono — di recente circa il doppio. I miner generano circa 450 BTC al giorno; i soli veicoli quotati, secondo Bitwise, rischiano di assorbire nell’arco del 2026 oltre il 100% dell’intera emissione dell’anno — una dinamica domanda-offerta che non ha precedenti nella storia dell’asset. Da una parte chi possiede l’asset lo toglie dal mercato e lo tiene. Dall’altra chi dovrebbe possederlo accumula promesse di dollari.

Non serve aggiungere altro. I due comportamenti, messi uno accanto all’altro, sono il vero grafico di questa nota.

VI. Give Bitcoin back to the people

Viene allora da chiedersi dove sia finita la promessa. La libertà finanziaria, l’autosovranità, il vecchio HODL, l’etica cypherpunk da cui tutto questo è partito. Sono stati corrotti?

La nostra risposta è no. Non sono stati corrotti. Sono stati resi scomodi.

I principi non sono stati toccati nel codice. Il protocollo è esattamente quello di sempre: la scarsità c’è, l’autocustodia funziona, nessuno l’ha smontata — anzi, oggi è più diffusa che mai. E ha una data di nascita precisa: nel novembre 2022, nel mese del crollo di un grande exchange, oltre 325.000 BTC lasciarono le piattaforme in poche settimane. Fu la paura a insegnare alle persone a custodire da sé. Da allora il movimento non si è più fermato — ed è proprio per questo che le riserve sugli exchange continuano a crollare. Ciò che è cambiato non è la possibilità. È il default. Un tempo la sovranità era l’unica strada disponibile. Oggi è una delle due, ed è quella più faticosa: quella che devi scegliere con intenzione, contro la corrente della comodità che ti spinge verso il dollaro sintetico a ogni passo.

È questo il vero campo di battaglia. Non tra Bitcoin e le banche. Tra la comodità e l’intenzione. La fregatura in atto non è un complotto: è una deriva, mille piccole scelte comode che, sommate, riconsegnano il numéraire proprio al sistema fiat che Bitcoin era nato per superare.

Per questo lo diciamo chiaro, e lo diciamo a chi ci legge prima ancora che ai mercati: give Bitcoin back to the people. Ridate Bitcoin alle persone — e ridatelo nell’unica forma che conta, quella in cui Bitcoin è il metro, non l’oggetto da prezzare in dollari. Tornate a contare in sats. Tornate a togliere dal tavolo e a custodire. Tornate a leggere il grafico invece del post.

La scomodità non è una condanna. È una scelta. E ogni stack di sats, oggi, è quella scelta resa concreta.

La Federation è un collettivo di ricercatori e builder Bitcoin indipendenti. Parlo a suo nome. Non riveliamo i membri — è il lavoro a parlare.