Thirty Days, Thirty Ticks

Federation Research Note # 2 — SATSINDEX Federation — May 2026

🇬🇧 Read in English · 🇮🇹 Leggi in italiano

Thirty Days, Thirty Ticks

1. The Question

There’s an old question, one of those that circulates in bars and behavioural finance classes. It goes like this.

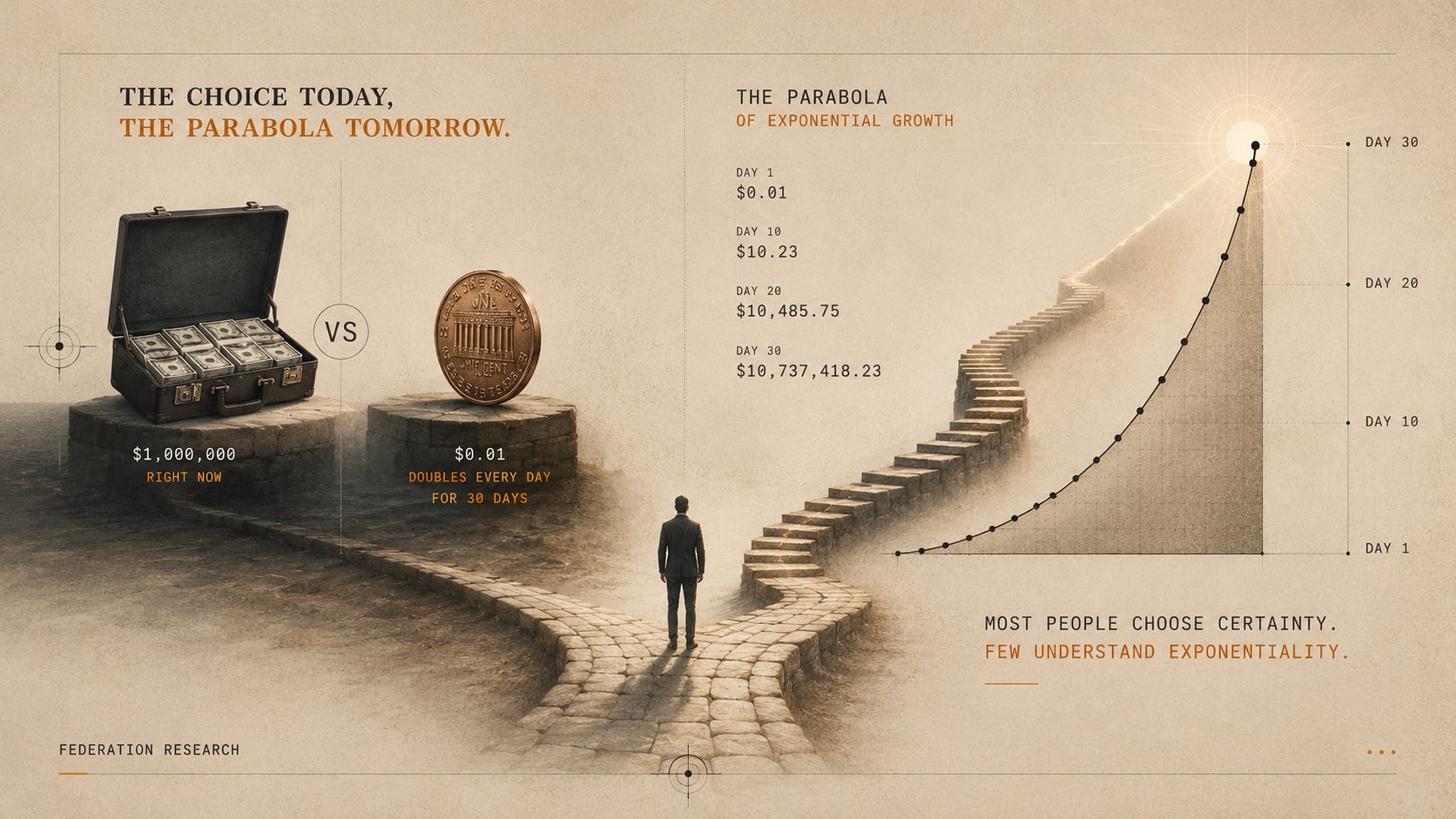

Would you rather have one million dollars right now, in cash — or one cent that doubles every day for thirty days?

Stop for a moment. Don’t scroll. Don’t jump to the line below.

Answer with the first thing that came to your mind.

2. The Reaction

If you are like the ninety-nine per cent of people we have asked this question, you answered the million. And you answered quickly.

We know this because we have asked. In private, to friends, to clients, to relatives. The answer is always the same, and almost always arrives with the same tone: half-amused, half-irritated, as if the question were some beach-quiz trick. Of course the million, what kind of question is that. Some add a justification, sensing that the speed of the answer needs explaining: a million now is a million now, no jokes, I put it in the bank and sleep well. Others just laugh.

There is nothing stupid about this reaction.

From the Federation angle, however, we hold that finance must be studied by observing how the mind works, not how it should work. And the human mind — the one that has read Descartes, built computers, sent probes to Mars — has been trained over fifty thousand generations for a much older task: estimating small quantities, counting them, summing them. Recursive multiplication — what economists call compound interest, and what mathematics calls the exponential function — is a recent invention, and our brain handles it with a clumsiness that would make an eight-year-old smile in front of a calculator.

This clumsiness has a name. It is called the linearity bias, and it has been documented for forty years in the academic literature. The mind projects forward by adding, not by multiplying. It sees a sequence and imagines a straight line. When you present it with a curve, the line it has drawn in its head deceives it until the last possible minute.

Now let us do the math. Really, from scratch, as if we had never heard the question.

3. The Demonstration

Let us settle in. No algebra, no powers, no exponents. Just a column of numbers.

A cent is zero point zero one dollars. $0.01. Tomorrow it doubles, and becomes $0.02. The day after, again, and becomes $0.04. And so on for thirty days.

A reading note before we begin, because the trap starts right here. In the right-hand column you will read what is paid to you on that specific day. Not the total accumulated. The total we note separately, under each decade, because that is the number that really counts — and it is the one the mind forgets to sum as it reads.

First decade

| Day | Payment |

|---|---|

| Day 1 | $0.01 |

| Day 2 | $0.02 |

| Day 3 | $0.04 |

| Day 4 | $0.08 |

| Day 5 | $0.16 |

| Day 6 | $0.32 |

| Day 7 | $0.64 |

| Day 8 | $1.28 |

| Day 9 | $2.56 |

| Day 10 | $5.12 |

Total accumulated at end of day 10: $10.23. Ten dollars and twenty-three cents. After one-third of the bet. You’d want to call the friend who proposed this game and tell him you’ve been a fool not to take the million. Don’t call him yet. Wait.

(A note on the math, valid for all the decades that follow: the accumulated total is the sum of every day up to that point, current day included. At the end of day 10 you have today’s $5.12 plus the $5.11 accumulated over the previous nine days: $5.12 + $5.11 = $10.23. There is a regularity worth noting just once: the sum of all previous days always equals the last payment minus one cent. Once you grasp the mechanism here, it holds for every box that follows.)

Second decade

| Day | Payment |

|---|---|

| Day 11 | $10.24 |

| Day 12 | $20.48 |

| Day 13 | $40.96 |

| Day 14 | $81.92 |

| Day 15 | $163.84 |

| Day 16 | $327.68 |

| Day 17 | $655.36 |

| Day 18 | $1,310.72 |

| Day 19 | $2,621.44 |

| Day 20 | $5,242.88 |

Total accumulated at end of day 20: $10,485.75. Ten thousand dollars and change. After two-thirds of the bet. Your friend, meanwhile, has already invested the million: he bought a new car, made a down payment on a house, opened a savings account. You are sitting on just over ten thousand — barely one per cent of the million you refused — and you’d start seriously thinking you chose wrong. Hold on.

Third decade

| Day | Payment |

|---|---|

| Day 21 | $10,485.76 |

| Day 22 | $20,971.52 |

| Day 23 | $41,943.04 |

| Day 24 | $83,886.08 |

| Day 25 | $167,772.16 |

| Day 26 | $335,544.32 |

| Day 27 | $671,088.64 |

| Day 28 | $1,342,177.28 |

| Day 29 | $2,684,354.56 |

| Day 30 | $5,368,709.12 |

Total accumulated at end of day 30: $10,737,418.23. Ten million, seven hundred thirty-seven thousand dollars and twenty-three cents.

Now stop. Re-read that number.

The thirtieth day alone — one day, twenty-four hours — paid you five million three hundred sixty-eight thousand dollars. More than five times what your friend received at the start. In a single day.

And the cumulative total is almost eleven million.

4. The Reversal

Ninety-nine per cent of the people we ask choose the million. Sure of themselves. Convinced. Relieved, even, for having avoided the trick. They have chosen, in exact proportion, one-tenth of what they could have had. They have left $9,737,418.23 on the table.

Almost ten million. Convinced they were clever.

From this side — the Federation angle, that of Federation Research — what interests us is not laughing at those who choose badly. What interests us is understanding why the human mind chooses, systematically, repeatedly, predictably badly in this kind of bet. Because the same pattern will repeat later on, on a different scale, with a different asset. And we want those who read these lines, when the pattern presents itself again, to recognize it.

Look at the sequence of totals at the end of each decade:

End of day 10 → $10.23

End of day 20 → $10,485.75

End of day 30 → $10,737,418.23

Every ten days, three zeros are added to the cumulative total. Three clean zeros. The pattern is written in round figures, but in the first two-thirds of the bet it is practically invisible to the linear mind. Only in the last third does it explode.

And there is a yet more uncomfortable detail, which the Federation considers the true heart of the paradox. After twenty-six days — eighty-seven per cent of the time of the bet, nearly all of it — you are still at $671,088.63. You haven’t yet reached the million. Your friend looks at you with pity.

It is on day twenty-seven that you surpass him, and only just. From day twenty-eight onward, something happens that the linear mind cannot foresee: in the last three days you earn seven times all that you had accumulated in the previous twenty-seven. Ninety per cent of the time of the bet produces one-eighth of the final result. The last ten per cent of the time produces the remaining seven-eighths.

And there is a still sharper regularity, worth fixing because we will return to it. Each day you remove from the end, the cumulative total halves. On day 29 you have half. On day 28 a quarter. On day 27 one-eighth. On day 26 one-sixteenth. On day 25 one-thirty-second. The parabola contains its entire history compressed into the last step. All of it. The story of the bet is written in its last day, and in no other.

When we look at Bitcoin today and someone says “it’s too late, it has already risen too much”, they are saying something the penny paradox flatly contradicts: in geometric growth, the last step contains half of the game. The fact that the previous steps have already been climbed does not reduce the next one — it enlarges it.

Our federative view holds that this is not a mathematical exercise. It is an anthropological theorem. It states that the human species, faced with geometric growth, cannot believe its own luck until the second-to-last useful moment. And when it manages to believe, it has usually already chosen the other option.

Now that the penny paradox is clear, we can do the interesting thing: ask whether there exists, in the real world, an asset that behaves exactly this way.

5. What If It Were Bitcoin?

There exists a real asset that behaves like the penny of the parabola.

It is called Bitcoin, and it has its own minimum unit — the one that, in the ratio between a whole Bitcoin and its smallest fraction, occupies the same position the cent occupies in the ratio with the dollar. It is called satoshi, after the name of its inventor, and for fifteen years the industry that should have explained it has done its best not to.

It has presented it like this: 0.00000935 BTC.

Or like this: $0.000935.

Numbers with five, six, seven zeros before the first useful digit. Numbers that the human mind, simply, reads as nothing. It is not a defect of the reader — it is how the mind is made. It works with whole numbers, not with shattered decimals. The whole number is weighed, counted, pocketed. The leading zero vanishes like a breath.

Let us try it ourselves. Stop and do this experiment — even just in your head, but better if tomorrow you actually try it with someone.

Ask any person: how much do you have in your pocket right now?

They will answer, let’s say: a dollar. Or a euro. The figure doesn’t matter.

Now ask: in what other way could you call it?

Almost always they will look at you puzzled. Perhaps they will answer with another currency — a euro is about a dollar and change, a dollar is about ninety cents of a euro. Few, very few, will give the answer that from the Federation point of view we hold to be the correct one:

One hundred cents.

A dollar is one hundred cents. Same currency, same value, two different grammars. And yet the mind treats them as two different things: a dollar sounds like one unit, one hundred cents sounds like a small fortune. A hundred of something, in hand, always weighs more than one.

Now let us apply the same logic to Bitcoin.

Today, with a single dollar, you buy 1,070 satoshis.

Not zero point something. Not a decimal. One thousand and seventy. One thousand and seventy whole units, countable, accumulable, pocketable. The same dollar that, on the other side of the industrial grammar, was 0.00000935 BTC and looked like dust.

Everything changes. The way the mind registers the purchase changes, the way the mind registers possession changes, the way the mind imagines future growth changes. From this Federation angle, we hold that half of the popular misunderstanding of Bitcoin is a misunderstanding of units of measurement. People did not refuse Bitcoin because they did not understand the technology. They refused it because someone showed it to them in a grammar that the brain reads as irrelevant.

And now, with the correct grammar in hand, we can return to the penny paradox.

What happens if that cent of the bet is not just any cent — it is a satoshi?

What happens if the doubling parabola does not apply to a thought experiment closed in thirty days — but to a real asset, one that exists, that has already traversed a portion of its own parabola, and that has another portion still ahead?

To answer these two questions we must first fix two things: how big a satoshi is today, measured in dollars, and at what point of the parabola we find ourselves.

We will address them separately, in the next two sections, first over different horizons — three years and thirty years — and then over the long historical arc that begins in 2009.

6. The Parabola Applied to Bitcoin

Let us set aside dollars for a moment and reason in satoshis.

Today a satoshi is worth, in dollars, 0.000935. Five zeros after the decimal point before finding a useful digit. We have already seen this: it is the number the brain refuses to read.

But there is another grammar to say the same thing. We can ask: how much must a satoshi appreciate to be worth as much as a cent of a dollar? That is, to be worth $0.01 — a figure the mind reads as a whole unit, a real cent?

The answer is: the satoshi must rise by a factor of 10.7 times its value today. In other words, it takes just over three and a half doublings.

Three and a half doublings, let us remember, is what the penny paradox produces in three and a half days. For the satoshi, the path is not measured in days: it is measured in cycles. And here two horizons come on stage that the Federation considers fundamental to distinguish — one short, one long — because they speak to two very different kinds of reader and to two very different kinds of life project.

Horizon A — Three Years

Three years is the time arc of a single Bitcoin cycle. Between one halving and the next there are roughly four years; within this window are concentrated an accumulation phase, a price-explosion phase, a euphoria phase, and a correction phase.

If in the next cycle — the one that had its halving in April 2024 and that will unfold in the months following — the satoshi were to perform three and a half doublings, one satoshi would be worth as much as a cent of a dollar. Translated into the other grammar: one Bitcoin would be worth one million dollars. From that moment on, every dollar in the reader’s wallet would buy not 1,070 satoshis any longer, but 100.

The number of zeros would flip. The satoshi would cease to be “dust” and would become the new popular unit of account. The dollar itself, in fact, would be redenominated into satoshis in the head of anyone who has already made the paradigm shift.

This is Horizon A. Three years, three and a half doublings, and the penny paradox applied to Bitcoin closes evenly with the original paradox.

Horizon B — Thirty Years

Thirty years is the time arc of a working life. It is the accumulation plan that a twenty-five-year-old today can begin to build thinking of when they will be fifty-five. It is, from the Federation angle, the real horizon.

In thirty years, according to the cadence of the Bitcoin protocol, there occur about seven and a half halvings — seven ticks of the long metronome, the one that every four years halves the new supply of Bitcoin coming to market. Each halving, historically, has produced one to three doublings of price in the two or three years that followed. Let us keep here a prudent assumption: one structural doubling per halving.

Seven doublings in thirty years means a factor of 128 times the starting value. If today one Bitcoin is worth about $93,000, in thirty years — at our conservative assumption, a single multiplication by two every four years — it would be worth almost twelve million dollars.

Translated into satoshis in the pocket: today with one dollar you buy 1,070 sats; in thirty years, with the same dollar, you would buy about eight. Not two hundred, not five hundred. Eight satoshis. Each sat would therefore have become something worth, in proportion, what today is a ten-cent coin.

Now let’s take the perspective of the twenty-five-year-old who today sets aside one hundred dollars a month in Bitcoin. Twelve hundred dollars a year, at today’s prices, buys about one million three hundred thousand satoshis a year. In thirty years, almost forty million satoshis accumulated — that is, just under half a whole Bitcoin.

At $0.000935 per sat (today’s price), that half-Bitcoin is worth about $37,000. Practically the capital invested. Apparently, nothing gained.

But applying the conservative assumption of seven doublings in thirty years — the most cautious possible, the one that presupposes a drastic deceleration compared to all of Bitcoin’s history so far — those nearly forty million sats are worth in thirty years about four million seven hundred thousand of today’s dollars.

Four million seven hundred thousand dollars, from a sum invested of thirty-six thousand. One hundred thirty times the capital invested.

And remember: this is the conservative scenario. The one that presupposes that Bitcoin in the next thirty years will behave much, much worse than it has in the fifteen just passed.

A note of transparency. The calculations in this section are made at the price of Bitcoin at the moment this article was written — roughly $93,000 per Bitcoin, roughly 1,070 satoshis per dollar. The price is in continuous movement: when the reader reads these lines it will be different, perhaps a little, perhaps a lot. The logic of the parabola, however, does not change with the day’s price: what changes is the starting point, not the geometry of the path.

The Leap of the Linear Mind

Now the reader can do two things.

They can look at the final number — four million seven hundred thousand — and feel rising the same identical reaction of those who, faced with the penny paradox, answered the million, obviously. That is: too good to be true, there’s a trap somewhere, I don’t believe it.

Or they can look at the mechanism that produces that number — seven doublings in thirty years, one every four years, paced by a metronome that is written in the code of the protocol and has never missed a beat in sixteen years — and accept that there is no trap. There is only, again, the math of doubling, applied to a time horizon longer than the linear mind can imagine with ease.

The penny paradox lasts thirty days and produces eleven million. The satoshi paradox lasts thirty years and — in the most conservative assumption — produces a result of the same order of magnitude. Same geometry, on a different scale. Same theorem disguised as a riddle.

One question remains, and it is the most important. If the parabola of the satoshi is already in motion, at what point of the parabola are we today?

This question is the subject of the section that follows. And it is here that the Federation deposits its first Call with timestamp.

7A. Where We Are in the Parabola

Bitcoin is born on 3 January 2009, when Satoshi Nakamoto mines block number zero — the genesis block. For about eighteen months it has no market price: it is exchanged among enthusiasts as a technical curiosity, at par, with no monetary reference.

The first registered price dates from mid-2010: roughly three-tenths of a cent of a dollar per Bitcoin. Zero point zero zero three dollars. A Bitcoin was worth, literally, less than a tenth of a cent. At that price, a single dollar would buy roughly three hundred thirty thousand whole Bitcoins.

Today, sixteen years later, the same Bitcoin trades around $93,000.

Now let us do the only operation that matters: let us count the doublings that separate those two numbers. From $0.003 to $93,000 there is a growth factor of about thirty-one million times. To cover such a large factor with successive doublings requires — the math is elementary, just count how many times you multiply by two starting from one to arrive at thirty-one million — about twenty-five doublings.

Twenty-five.

Now go back mentally to the penny paradox. Thirty doublings in thirty days, eleven million dollars accumulated by the last. Twenty-five doublings was the number that corresponded, on our table, to day 25 of the bet. Let us see it, because it is important that the reader see it with their eyes and not only with their head.

At the end of day 25 of the penny bet, you have $335,544 in your pocket. More than three hundred thousand dollars. A respectable sum. A sum that, if you had been offered thirty thousand dollars on day one instead of the cent to double, would have seemed impossible.

But you still have five days of bet left. And in those five days the cumulative total goes from $335,544 to $10,737,418. Thirty-two thousand times as much. In five days.

Bitcoin, today, is exactly in this position. It has already traversed twenty-five price doublings: from its first market price to today, its value has doubled about twenty-five times. But be careful not to confuse two different things, because everything hinges on this. One is the price doubling — how many times the value multiplies by two. The other is the tick of time — the halving, the protocol’s heartbeat that paces the rhythm every four years. They are two distinct rulers, and they measure distinct things. How many price doublings lie ahead, no one can say by counting them: Bitcoin’s parabola is not read on the ruler of price, but on that of time. It is there — on the ticks of the halving — that we must look to know where we truly are.

To understand why, we must look at what scans, exactly, these doublings. The answer is a mechanism of the protocol that was programmed by Satoshi Nakamoto sixteen years ago, that has never missed a beat, and that every four years reminds us — with a precision that the linear mind struggles to digest — that the geometry of Bitcoin is not opinion, it is code.

7B. The First Federation Call

In Bitcoin, every four years approximately, a programmed event occurs that is called halving.

What is halved is the reward that the protocol pays to the miners, the people (and computers) that keep the network alive by validating transactions. When Bitcoin was born, every ten minutes the network created fifty new Bitcoins and gave them to the miners as the reward for their work. After the first halving, the reward dropped to twenty-five. After the second, to twelve and a half. After the third, to six and a quarter. After the fourth — the April 2024 one — to three and an eighth. Every four years, the supply of new Bitcoin entering the market halves.

Translated: scarcity doubles. And when scarcity doubles while demand does not fall, the price — by a law that is the first thing one studies in any economics manual — tends to rise. It has done so spectacularly in the four halvings so far, and there is reason to believe — for reasons the Federation will expand in dedicated volumes — that it will continue to do so in the ones to come.

The halving is the metronome of Bitcoin’s parabola. Exactly as the day is the metronome of the penny parabola. Every four years, one tick; every tick, one structural doubling of scarcity.

Now the point.

In the code of the Bitcoin protocol, written by Satoshi Nakamoto and never modified in sixteen years, there are programmed in total thirty-two halvings. Thirty-two halvings, scanned in time, after which the block reward will drop below the threshold of one satoshi and Bitcoin will cease issuing new units. The last halving will fall around the year 2140 — one hundred fourteen years in the future, beyond the duration of an entire human life counted from today.

But of these thirty-two halvings, two remain at the margins of the human parabola.

The first, occurred in November 2012, took place when the satoshi did not yet have an observable retail price. Bitcoin existed, but it was not yet pocket money for anyone outside a small technical community of cypherpunks, solitary miners, and curious academics. No shop accepted it, no retail app made it easy to buy, no mainstream newspaper covered it. That first halving occurred in a room that, monetarily, was still empty.

The last, expected in 2140, will fall beyond the duration of a human life counted from today. None of us who read these lines will see it, and none of us here needs to see it: the point of the parabola is that it completes itself, not that we watch it end.

In between, thirty halvings. Thirty ticks monetarily lived by the human species — exactly as many as the days of the penny paradox.

The penny paradox uses thirty days because that is the number the human mind holds: thirty steps that produce a finite, surprising, but intuitively verifiable figure. Bitcoin offers thirty observable halvings because that is the number the human species holds: thirty ticks of the metronome that traverse the retail history of the asset, from the beginning of its popular monetization to the point where the satoshi ceases to be divisible into whole units.

Coincidence that is also structure.

### Federation Call No.1

Bitcoin has exactly thirty days of the penny parabola ahead of it — thirty observable halvings, scanned in the code of the protocol, of which four already crossed. We are, literally, at tick 4 of 30 — four halvings out of the thirty observable ones. Not four price doublings: four beats of the metronome of time.

The penny paradox is a thought experiment. Bitcoin’s parabola is already in motion.

— Federation Research, 23 May 2026, on the Substack channel of Federation Research

And there is a further level, worth fixing briefly before closing this section — because it speaks of how Bitcoin keeps time, and introduces a precision that, once seen, is not forgotten.

Inside the halving — the long metronome, beating every four years — there are two shorter metronomes, nested like the gears of a mechanical clock.

The first is the block. Every ten minutes or so, the Bitcoin network produces a new block of transactions. Not every nine. Not every eleven. Every ten. It is written in the code and has been respected for sixteen years with a precision that no biological clock, no time zone, no central bank possesses.

The second is the difficulty adjustment. Every 2,016 blocks — about two weeks — the protocol recalibrates automatically: if miners have become more numerous and blocks come out faster than expected, the difficulty of the calculation increases; if miners have become less numerous and blocks come out slower, the difficulty decreases. In both cases, the ten-minute rhythm is restored.

Three nested clocks. The block every ten minutes. The difficulty every two weeks. The halving every four years. None of the three depend on governments, banks, opinions, wars, or time zones. Bitcoin has its own internal time, and that time cannot be negotiated.

Of the fine mechanics of this clock — of why it works, of why it has never missed a beat, of why it is the first true monetary time machine in human history — the Federation will speak in due time, in a dedicated volume.

For now, the Call is enough for us. And it is enough for us to know where we are.

Tick 4 of 30.

There is, however, one last observation we want to leave with the reader before closing this section. When we began this article, we chose the metaphor of the doubling cent because it is the simplest, most pedagogically tested way to explain geometric growth. Thirty doublings. Thirty days. Nothing particular in the choice of thirty: a number the human mind holds without too much effort, large enough to produce the final punch, small enough to be tabulated on a sheet of paper.

And yet, building the argument, we found ourselves in front of an observation that deserves to be fixed.

The thirtieth tick of Bitcoin’s halving — the thirtieth of the thirty observable in the human parabola of the satoshi — falls, according to the calculations of the protocol, around the year 2140. It is exactly the year in which the last block will be mined, in which the last satoshi will be issued, in which Bitcoin’s emission curve will reach its asymptote and will stop forever.

Thirty days in the pedagogical metaphor of the cent. Thirty ticks in the human parabola of the satoshi. The same number, in two places that have no apparent reason to speak to each other.

The Federation calls this phenomenon by the name mathematicians have always given it: the Beauty of Mathematics. That moment in which a geometric structure replicates itself across different scales of reality — pedagogical, economic, monetary — without anyone having designed it to do so.

Chance or structure? The question remains open, with the reader. We will return to it.

8. Why People Get It Wrong

Now that we have seen the penny paradox, and now that we have seen Bitcoin’s parabola overlap the same geometry, we can finally face the question that no finance manual openly addresses.

Why, exactly, do ninety-nine per cent of people choose the million?

It is not a single reason. There are seven, and they present themselves together, intertwined, in a few seconds. The mind makes the decision before consciousness arrives to call it to account. When consciousness arrives, it finds a choice already made and limits itself to justifying it — a phenomenon psychologists call retroactive rationalization, and it is the main reason we ask “why did you choose that?” and we get answers that are always coherent, always lucid, always wrong about the real cause.

Let us see them one by one. And for each, the Federation angle proposes the same logic applied to Bitcoin — because the same error that causes one to choose the million also causes one to sell Bitcoin at the worst moment.

First error — the greed of immediate time.

I want the million now, I don’t wait thirty days. It is the oldest voice in the human brain, the one behavioural psychology calls hyperbolic discounting: the tendency to value a future reward as drastically lower than the same reward now, even when the math says otherwise. The same logic applied to Bitcoin: I sell at +30%, I don’t wait for the end of the cycle. Same voice, same emotional scale, same structural loss.

Second error — overconfidence.

Obviously the million, not even worth asking. It is the certainty of someone who hasn’t yet done the math, and who declares “obvious” something they have just calculated in a tenth of a second. Confidence, in behavioural research, is the most reliable signal of a badly made decision — because someone who has truly calculated hesitates, and someone who has not calculated declares obvious. The same logic applied to Bitcoin: it’s already risen too much, it’s too late. Same certainty, same tenth of a second, same blindness.

Third error — the linear mind.

The brain sums, it does not multiply. It sees a sequence and imagines a line. In the penny paradox, after ten days about ten dollars has accumulated, and the mind projects linearly: thirty days will mean thirty dollars, or a little more. When it is revealed that the final result is eleven million, the mind cannot believe its eyes — not because the numbers are complicated, but because the mental structure that read them was not equipped to read them. The same logic applied to Bitcoin: I can’t conceive that the price could do another five doublings. It is the same straight line projected on the future of an asset that grows on a curve.

Fourth error — aversion to uncertainty.

A certain million beats thirty days of if. Even when the “if” is a bet with a mathematically determined outcome — the doublings are not uncertain, they are written in the rule of the game — the mind reads the future as generic uncertainty, and generic uncertainty as risk. The same logic applied to Bitcoin: better my euros in the bank, at least they are certain. The perceived certainty of the euro is, from the Federation angle, one of the greatest monetary illusions of our time — but we will speak of this in dedicated volumes. For now let us register the mechanism: in the mind, a certain but small win beats an uncertain but large win — even when the large win is written in the rule of the game and the uncertainty is only perceived.

Fifth error — recency bias.

The mind evaluates phenomena from the recent examples it has seen. In the paradox, it judges based on the low payments of the first days and generalizes to the rest. In Bitcoin, it judges from the price of the last six months and generalizes to the whole cycle. If Bitcoin has fallen thirty per cent in the last six months, the mind concludes it will continue to fall. If it has risen fifty, it concludes it will continue to rise. In both cases, the conclusion turns out almost always wrong — because the cycle is longer than the observation window, and the mind has no tools to read what it does not see.

Sixth error — loss aversion, in its three faces.

Daniel Kahneman and Amos Tversky won the Nobel Prize in Economics in 2002 by demonstrating something that, once seen, is not forgotten: losing something we have burns, in the human brain, about twice as much as the pleasure of gaining the same thing.

In the penny paradox, this asymmetry operates transparently: the million, once visualized as possessed, becomes something not to lose — and the parabola of eleven million, not yet visualized, cannot compete.

The same logic applied to Bitcoin manifests itself in three faces — and here the Federation proposes a distinction that behavioural literature usually does not handle. Because the first two faces are market behaviours, and economists study behaviours. The third is a pure state of the human soul, and economists do not know where to put it.

The first face is the most known. The thirty per cent drawdown burns twice as much as the subsequent one hundred per cent gain. The small investor sells at the lows — the pain of the open loss pushes him out, exactly at the moment when he should stay in. Whoever sells at the lows carries a recoverable pain: the asset, sooner or later, rises again. Bitcoin’s history confirms this in every past cycle. It is acute pain, but it is pain with a future.

The second face is its mirror. When the trader sees Bitcoin rise without being positioned, and cannot bear the burn of being out of the market, he ends up entering at the wrong price — with the wrong position, with the wrong sizing, with discipline suspended. The hurry is not pursuit of gain: it is flight from a pain. This too, like the first, is a market action — a concrete, recordable, accountable move.

The third face is the one almost no one talks about, and from the Federation angle it is the most painful of all. It is the pain of one who watches Bitcoin rise without being inside, and does not enter. He does not sell badly, he does not buy badly, he does nothing. He stands at the side of the road as the train passes, watches it move away, and understands — with a lucidity that always arrives too late — that that specific train will not return.

Bitcoin at nine thousand dollars, today, is an event that will not be repeated. Bitcoin at ninety thousand, in ten years, will be remembered the way today we remember Bitcoin at nine thousand. Whoever is inside during a drawdown carries pain that time can heal. Whoever has entered badly at a peak carries pain that discipline can, at least, account for. But whoever remains outside during a structural rise carries pain that is irrecoverable, pain that time does not heal and no subsequent action can repair. The past level does not return. The next cycle will open another door. Not the same one.

For this reason, from the Federation angle, the third face is the most insidious. The first two are errors of execution: one can train oneself to recognize them and contain them. The third is an error of presence: one can only, banally, be there. Bitcoin does not ask the reader to guess the price. It asks him to be there in time.

The same bias, then, a single architecture, three faces. Two wrong actions and one non-action that burns more than both. The Bitcoin protocol, indifferent to human emotionality, brings all three into evidence with a clarity few other assets possess.

Seventh error — anchoring, the price the mind does not let go.

The human mind has a technical defect in the way it evaluates numbers: it anchors itself to the first number it encounters, and from there on measures everything else in relation to that anchor — even when the anchor no longer has any relation to the reality it is trying to evaluate. It is the most documented bias in behavioural literature, yet it is also the most difficult to disarm, because it operates silently, beneath the threshold of awareness.

In the penny paradox, the anchor is precisely the “million” of the initial question. When the reader hears a million dollars now, the number plants itself in the mind as a reference for “a lot”, and everything proposed in alternative is measured against it. Even when one discovers that the parabola produces eleven million, the mind struggles to accept that eleven million is truly eleven times as much — because the anchor of the million resists, and disguises itself as the threshold of “reasonable wealth”.

The same logic applied to Bitcoin produces one of the most frequent, and most costly, behaviours in the recent history of the market.

Whoever saw Bitcoin at twenty-five thousand dollars in 2022 struggles to buy it at ninety-three thousand in 2026. Not because ninety-three thousand is objectively “expensive” — the evaluation of expensive or cheap requires a model, a comparison, a time horizon, and almost no one does this work. He struggled to buy it for a much simpler reason: he has an anchor, and the anchor is the price he saw the first time. Everything above the anchor seems “too expensive”. Everything below it seems “a good deal”. And so he waits, and waits, and waits — until the anchor recedes so far that it becomes ridiculous, and at that point, finally, he enters. Almost always near the next peak, when a new anchor — higher — has already formed in his head.

The Federation angle proposes an observation that, once seen, dismantles the bias from its foundations: in an asset that moves on a long-period parabola, every anchor is destined to become obsolete. Bitcoin at twenty-five thousand was the anchor of 2022. Bitcoin at ninety-three thousand is the anchor of 2026. Bitcoin at one million will be the anchor of some future year. None of these anchors is worth more than the others as a reference for “expensive” or “cheap”. They are all worth as photographs of a single moment in the parabola — and the moment is not the price. The moment is the point of the path.

Whoever buys anchoring himself to the past price is making, fundamentally, the same mistake as whoever looked at the penny paradox after ten days and said “ten dollars, that’s ridiculous”. He was measuring a parabola with the ruler of a single point, and the ruler — by definition — cannot read a curve.

The Diagnosis Before the Cure

Seven errors, seven manifestations of one and the same mental architecture two hundred thousand years old, presenting itself in the twenty-first century with a different disguise but the same skeleton. They were the errors that made one choose the million against the parabola. They are the same that today make one sell Bitcoin at the lows, buy it at the highs, ignore it at the structural entry points, and rationalize every move with arguments that seem lucid but that are — almost always — justifications built after the decision.

From the Federation point of view, recognizing these errors is not a cure. It is a first diagnosis. Knowing that the linear mind will betray you, knowing that the anchor will distort your perception, knowing that the third face of loss aversion will keep you outside exactly the train you should take — does not mean you will stop making mistakes. It means that, next time you are about to do so, you will feel a small alarm inside your head. I’m making error number four, you will tell yourself. I’m making the six. I’m making the third face of the six.

That alarm, for many, is already enough. For others something more is needed — a method, a discipline, a system that recognizes errors before they manifest themselves and disarms them at the source. Of this method we will speak in dedicated volumes. But there is a question that precedes the method, a question that the reader — now that he has seen all the errors in a row — will want to ask almost inevitably.

If I have to enter Bitcoin, when do I enter?

The Federation answer to this question is less obvious than it seems.

9. When to Enter

If I have to enter Bitcoin, when do I enter?

Now. Yesterday.

These are the two answers the Federation gives to this question, and they are both correct. Now because the protocol is designed to serve whoever enters at any level, at any moment of their life cycle, regardless of the day’s price. Yesterday because every minute that passes is a minute more of parabola completing itself without the reader participating in it — and minutes, unlike prices, do not retrace.

This is not financial advice. It is a structural observation. And it is the same observation the penny paradox has already made obvious, for whoever has reached this line: in a parabola of thirty ticks with four ticks already crossed, there is no “right” moment to enter. There is only the moment when one enters.

Whoever entered at one dollar in 2011 and whoever will enter at three hundred thousand in 2027 are buying the same thing: a fraction of the same parabola, of which they still have ahead the same residual doublings. Neither of them has the right price. They both have their price — the price of the moment when they decided to be present.

The protocol does not discriminate on the price of entry. It discriminates on time in the system. It is a distinction the linear mind struggles to digest, because the traditional financial market has trained us for generations to ask “at what price do I buy?”. Bitcoin shifts the question ninety degrees: “from what moment am I in?”. The right answer to that question — the only answer the protocol recognizes — is a date, not a number.

And it is for this reason that the Federation, to whoever asks when do I enter, answers with two words that are apparently tautological and in reality exact: now, yesterday.

Of the complete mechanics of this principle — of why time in the market systematically beats timing the market, of why a regular accumulation plan disarms five of the seven errors we have just seen, and of why the Federation considers DCA not a strategy but a mental hygiene — we will speak in due time in dedicated volumes.

For now, it is enough to know that the question when to enter is the wrong question. The right question is another. And it has to do with something that, up to this line, we have taken for granted without ever naming it: what, exactly, is Bitcoin.

10. The Seal, the Judgement, the Choice

Now that the penny paradox has been seen, and now that its geometry has been overlapped on Bitcoin’s parabola tick by tick, only one thing remains to be done to close the picture. To understand what makes possible Bitcoin’s parabola to continue — and why, from the Federation point of view, the question when to enter is less important than the question the reader has not yet asked.

What does the reader decide, when he decides to be present or absent in this parabola?

The Seal

Bitcoin has a property that, before 2009, no monetary asset in human history had possessed. It is written in the first lines of Satoshi Nakamoto’s software, has never been modified, and is not negotiable.

Never more than twenty-one million Bitcoin. Never. Under no circumstance. For no reason.

It is not a political promise — political promises break. It is not a geological scarcity — geological scarcities are circumvented with technology. It is a mathematical seal, coded in such a way that any attempt to modify it would automatically produce a network different from Bitcoin, recognizable as such, rejected by all the honest nodes of the system.

Gold has a supply that grows, on average, one per cent per year. It seems little — on a thirty-year horizon it means that every ounce today will be diluted by a third of new supply that did not exist. Fiat currencies have unlimited supply, and the history of the twentieth century is the chronicle of the consequences of this unlimitedness. The shares of a company can be diluted — all it takes is a vote by the board to authorize a capital increase. Real estate can be built — more concrete, more apartments, more supply.

Bitcoin no. Never. For the first time in history, humanity has an asset that, by mathematical construction, cannot be inflated. The penny parabola could continue beyond thirty days if only someone added days to the bet. Bitcoin cannot add units to its supply. The end of the parabola is written.

The Judgement

An asset with fixed supply and variable demand produces a phenomenon that economic theory has known since Adam Smith: when demand rises and supply cannot respond, the price is the only variable that can adjust. It rises.

But there is something more subtle, and from the Federation angle it is what really counts. An asset with fixed supply is a mirror of the collective behaviour of those who hold it. In an asset with variable supply — the dollar, gold, shares — when someone sells, total supply remains unchanged and someone else buys. In an asset with fixed supply, every sale is a net transfer from one holder to another. Nothing is created, nothing is destroyed, everything moves.

The Bitcoin protocol, in fact, does one thing in time: it transfers wealth from the impatient to the patient. Not for moralism. For mechanics. Whoever sells at the lows hands his satoshis to whoever stays inside. Whoever is overwhelmed by panic cedes his position to whoever is capable of not reacting. Whoever chases speculative yields on platforms that then collapse gifts his capital to whoever holds everything in self-custody and does not sign transactions he does not need.

No human judge issues these sentences. The protocol issues them, mechanically, twenty-four hours a day, seven days a week, for sixteen years. It is a blind and perfectly coherent judgement: it does not evaluate intentions, it evaluates behaviours. It rewards whoever stays in the system. It penalizes whoever enters and exits emotionally. It completely ignores whoever stays outside — that is another form of penalty, but it is not the protocol that inflicts it. Time inflicts it.

The Choice

At this point of the article, the reader knows more than the majority of people who today own — or do not own — Bitcoin. He knows the penny paradox. He knows the geometry of the thirty doublings. He knows the coincidence of 2140. He knows the seven errors the human mind commits in the face of exponential growth. He knows the three faces of loss aversion. He knows the seal of the twenty-one million and the mechanical judgement of the protocol.

To know these things, from the Federation point of view, is already a position. One does not go back to being ignorant after having seen a theorem. Once the penny paradox has been understood, the reader cannot — even if he wants to — look at Bitcoin in the same way. The gaze has changed.

One decision remains, and it is the most personal of all. It is not the decision whether Bitcoin will rise or fall in the coming months: that is a prediction, and predictions are not the Federation’s business. It is not even the decision when to buy: that has already been resolved in the previous section — now, yesterday. It is a decision on a completely different plane.

It is the decision about who to be, now that one has seen.

There exist, from the Federation angle, two categories of readers who conclude this article. The first is that of whoever has seen the paradox, has seen the protocol, has seen the biases — and now will act. Not necessarily with large sums, not necessarily with complicated plans. Perhaps only by opening a small account, buying his first satoshi, setting aside one hundred dollars a month in an accumulation plan. Becoming present in the system, with that minimal form of presence the protocol is able to recognize and reward in time.

The second category is that of whoever has seen, has understood, has nodded — and then will let it pass. Not because he has not understood. Precisely because he has understood. Because the linear mind, faced with a decision that requires breaking inertia of years, prefers to stay still. Even when knowing that one should move has already become a pain — that third pain, the irrecoverable one, that we spoke of.

To these two categories of readers the Federation has only one thing to say — and it is not advice, it is not exhortation, it is not a sale. It is an observation that takes up, to close it, the frame we opened thirty days ago in the penny paradox:

### Thirty ticks. Four done. The next one is yours.

11. A Shadow That Returns

Whoever knows technical analysis will already have recognized, beneath the lines of this bet, a familiar silhouette. In the 1930s, an American accountant named Ralph Nelson Elliott, confined to bed by a long illness, spent seven years staring at stock charts searching for a regularity. He found it. He discovered that every impulsive market movement is composed of five waves, and that the third of these — almost always the longest, always the most explosive — is the one that overturns the perception of whoever is watching from outside. Waves one and two almost no one sees; the three arrives and overwhelms everyone.

The penny paradox does not depict a real market — it is too clean, too regular, it lacks the intermediate corrections. But the curve it draws in its last three days is the same identical psychological curve of an extended third wave: the moment in which the linear mind, after doubting for twenty-six days, ceases to be able to catch up.

Of the structure of Elliott applied to Bitcoin cycles we will speak in due time, in a dedicated volume. For now it is enough to fix one thing: the penny paradox is not an isolated case, and it is not a quiz trick. It is a theorem disguised as a riddle, and it is the same theorem that replicates itself on a much larger scale every time a finite-supply asset meets rising demand. Bitcoin is one case. It is not the only one. It is only the most transparent.

12. A Game to Play Before Closing

Before leaving you to the final stele, a game — identical in spirit to the one of the cent, with the same rules of the math of doubling. Only applied to Bitcoin, and only to the ticks that remain.

At the peak of October 2025, Bitcoin touched roughly one hundred twenty-six thousand dollars. From there on, according to our Federation Call, there remain to traverse between twenty-six and twenty-eight ticks of the parabola — depending on whether one counts the human parabola of the satoshi (30 total) or the entire protocol (32 total). For the game we will use the conservative value: twenty-six.

Now let us choose a multiplier per tick. Historically, every halving of Bitcoin has produced between two and five doublings of price in the subsequent cycle. For the game we will use two hypotheses, both lower than the historical average.

Hypothesis A — conservative: for each tick, the price multiplies by two.

You have already been warned that this is a prudent hypothesis. The history of Bitcoin has never respected it downward — it has always exceeded it. But let us play conservatively.

One hundred twenty-six thousand dollars, multiplied by two, twenty-six times in a row, makes eight and a half trillion dollars per Bitcoin in 2140. Eight followed by twelve zeros.

Hypothesis B — less conservative: for each tick, the price multiplies by three and a half.

This is still below the historical average of the first four eras of Bitcoin. Nothing hyperbolic.

One hundred twenty-six thousand dollars, multiplied by three and a half, twenty-six times in a row, produces a number the linear mind no longer knows how to read — sixteen quintillion dollars. Sixteen followed by eighteen zeros.

At this point stop. The numbers cease to mean anything.

And here the Federation takes a step back to be honest.

Those numbers, in dollars, are not predictions. They are mathematical artifacts — what the formula of doubling produces when you apply it to a long horizon. And there are two precise reasons why they should not be taken literally.

The first is that no asset, in any human history, has ever sustained a doubling for twenty-six consecutive cycles. Bitcoin will probably decelerate: the next ticks will be powerful, the last ones modest, up to an asymptote. Reality will be smaller than both our estimates.

The second is more important, and from the Federation angle it is the key. The dollar itself is not written in the protocol. Bitcoin is. To project a 2026 dollar one hundred fourteen years into the future is like asking what an Italian lira of 1911 is worth in 2026. It no longer answers anything real. The dollar we use today as a unit of measurement, in one hundred fourteen years, may no longer exist — or exist as one of many regional currencies, as has already happened to the Dutch florin after its century of dominance, and to the British pound after its own. Global reserve currencies, historically, last about a hundred years. The dollar has just finished its.

So let us redo the game — this time in gold.

Gold is the only monetary unit of measurement with which we can, today, speak to the reader of 2140 without risking speaking in Italian lira. It is measurable, it is verifiable, and it is practically certain it will still exist.

In October 2025, with gold around two thousand seven hundred dollars an ounce, one Bitcoin was worth approximately forty-six ounces of gold.

Hypothesis A (×2 per tick, conservative): one Bitcoin in 2140 would be worth approximately three billion ounces of gold.

Now the reality check. The total gold ever mined on planet Earth, from the first Egyptian mines until today, is approximately six billion three hundred million ounces. Six billion three hundred million — according to the World Gold Council data, the recognized authority on the subject.

Translated: in the conservative hypothesis, a single Bitcoin in 2140 would be worth approximately half of all the gold ever mined on the face of the Earth.

The number is mathematically correct. But it reveals a truth worth fixing, and it is the same truth the math has been telling us since Section 10. Bitcoin, at a certain point of its parabola, ceases to be measurable in other assets — because it becomes the unit of measurement itself.

When humanity reaches the point where it asks “how much is this house worth in Bitcoin?” instead of “how much is one Bitcoin worth in dollars?”, the parabola will have completed its work. And that point, from the Federation angle, is structurally inevitable in an asset with fixed supply and growing demand.

And now, the final argument against those who say Bitcoin is in a bubble.

A bubble is a phenomenon in which the price of an asset rises beyond its structural value, inflated by speculation, and then bursts returning to the mean. To define a bubble, two things are needed: a structural value of reference, and a measurable deviation from that value.

Bitcoin has no structural value of reference, because it is not a traditional asset. It does not generate cash flow (it cannot be valued with discounted cash flow). It is not anchored to a physical commodity (it cannot be valued in dollars per ton). It does not represent real property (it cannot be valued in square metres). It is pure monetary value, coded in mathematical scarcity. Its valuation is given, exclusively, by the equilibrium between a variable global demand and a fixed supply.

Whoever speaks of “Bitcoin bubble” is using a vocabulary that does not apply to the phenomenon. It is like saying “gold is in a bubble” in 1913, when the dollar was still anchored to gold. The question makes no sense, because the term of comparison is missing.

Bitcoin does not rise because it is inflated. It rises because supply cannot respond. It is exactly the opposite of a bubble: it is the first currency in human history that the market cannot deflate, because no one — no banker, no government, no board of directors — can increase its supply.

The satoshi parabola, in its twenty-six remaining ticks, is not a bubble. It is the orderly end of the first incorruptible monetary experiment in history. And whatever the exact number it will reach — in dollars, in ounces of gold, in any other unit — the geometry that produces it is already written. All that remains to be done is to be there or not to be there.

13. Thirty Ticks

We started from a bar question.

We made it into thirty days of math, a penny parabola, a seal of twenty-one million, a metronome of four years, seven errors of the one who watches, three faces of an ancient pain, a coincidence between 2140 and a number that pedagogy had chosen without knowing it, and a game with numbers the linear mind no longer knows how to read.

To whoever has reached the end, the Federation has nothing to add.

Coincidences that bear the weight of three independent observations, we said elsewhere in this article, are the beginning of something that deserves to be studied.

Studying is free. Being in time is not.

Thirty days in the paradox.

Thirty ticks in the parabola.

Four ticks have already passed.

The other twenty-six pass anyway.

This document is distributed free of charge as part of the Federation editorial series. Reproduction in whole or in part is permitted subject to citation of the source. The views expressed do not constitute financial advice. For in-depth analysis on the topics introduced here, please refer to the volumes of the SATSINDEX Federation Research series.

The Federation is a collective of independent Bitcoin researchers and builders. I speak on its behalf. We don’t disclose membership — the work speaks for itself.

Trenta giorni, trenta tic

Federation Research Note # 2— SATSINDEX Federation — Maggio 2026

1. La domanda

C’è una domanda vecchia, di quelle che girano nei bar e nei corsi di finanza comportamentale. Suona così.

Preferiresti un milione di dollari oggi, subito, in contanti — oppure un centesimo che raddoppia ogni giorno per trenta giorni?

Fermati un momento. Non scorrere. Non saltare alla riga sotto.

Rispondi con la prima cosa che ti è venuta in mente.

2. La reazione

Se sei come il novantanove per cento delle persone a cui questa domanda viene posta, hai risposto il milione. E hai risposto in fretta.

Lo sappiamo perché l’abbiamo chiesto. In privato, ad amici, a clienti, a parenti. La risposta è sempre la stessa, e quasi sempre arriva con lo stesso tono: un po’ divertito, un po’ infastidito, come se la domanda fosse un trabocchetto da quiz da spiaggia. Ma certo il milione, che domanda è. Qualcuno aggiunge una giustificazione, perché sente che la fretta della risposta va spiegata: un milione adesso è un milione adesso, non si scherza, lo metto in banca e dormo tranquillo. Altri ridono e basta.

Non c’è niente di stupido in questa reazione.

Dall’angolazione federativa, però, riteniamo che la finanza si studi guardando come la mente funziona, non come dovrebbe funzionare. E la mente umana — quella che ha letto Cartesio, costruito i computer, mandato sonde su Marte — è stata addestrata per cinquantamila generazioni a un compito molto più antico: stimare quantità piccole, contarle, sommarle. La moltiplicazione ricorsiva — ciò che gli economisti chiamano interesse composto, e che la matematica chiama funzione esponenziale — è un’invenzione recente, e il nostro cervello la maneggia con una goffaggine che farebbe sorridere un bambino di otto anni davanti a una calcolatrice.

Questa goffaggine ha un nome. Si chiama bias di linearità, ed è documentata da quarant’anni nella letteratura accademica. La mente proietta in avanti sommando, non moltiplicando. Vede una sequenza e immagina una retta. Quando le presenti una curva, la retta che ha disegnato in testa la inganna fino all’ultimo minuto possibile.

Adesso facciamo i conti. Davvero, da capo, come se non avessimo mai sentito la domanda.

3. La dimostrazione

Mettiamoci comodi. Niente algebra, niente potenze, niente esponenti. Solo una colonna di numeri.

Un centesimo è zero virgola zero uno dollari. $0,01. Domani raddoppia, e diventa $0,02. Dopodomani ancora, e diventa $0,04. Avanti così per trenta giorni.

Una nota di lettura prima di partire, perché la trappola comincia qui. Nella colonna a destra leggerai quanto ti pagano in quel giorno specifico. Non il totale accumulato. Il totale lo annotiamo a parte, sotto ogni decade, perché è il numero che davvero conta — ed è quello che la mente dimentica di sommare mentre legge.

Prima decade

| Giorno | Pagamento |

|---|---|

| Giorno 1 | $0,01 |

| Giorno 2 | $0,02 |

| Giorno 3 | $0,04 |

| Giorno 4 | $0,08 |

| Giorno 5 | $0,16 |

| Giorno 6 | $0,32 |

| Giorno 7 | $0,64 |

| Giorno 8 | $1,28 |

| Giorno 9 | $2,56 |

| Giorno 10 | $5,12 |

Totale accumulato a fine giorno 10: $10,23. Dieci dollari e ventitré centesimi. Dopo un terzo della scommessa. Vorresti chiamare l’amico che ti ha proposto il gioco per dirgli che sei stato un cretino a non prendere il milione. Non chiamarlo ancora.

(Una nota sul calcolo, valida per tutte le decadi che seguono: il totale accumulato è la somma di tutti i giorni fino a quel punto, giorno corrente incluso. A fine giorno 10 hai i $5,12 di oggi più i $5,11 accumulati nei nove giorni precedenti: $5,12 + $5,11 = $10,23. C’è una regolarità che vale la pena notare una volta sola: la somma di tutti i giorni precedenti è sempre pari all’ultimo pagamento meno un centesimo. Una volta capito il meccanismo qui, vale per ogni box successivo.)

Seconda decade

| Giorno | Pagamento |

|---|---|

| Giorno 11 | $10,24 |

| Giorno 12 | $20,48 |

| Giorno 13 | $40,96 |

| Giorno 14 | $81,92 |

| Giorno 15 | $163,84 |

| Giorno 16 | $327,68 |

| Giorno 17 | $655,36 |

| Giorno 18 | $1.310,72 |

| Giorno 19 | $2.621,44 |

| Giorno 20 | $5.242,88 |

Totale accumulato a fine giorno 20: $10.485,75. Diecimila dollari e qualcosa. Dopo due terzi della scommessa. Il tuo amico, intanto, il milione l’ha già investito: si è preso una macchina nuova, ha versato l’acconto su una casa, ha aperto un conto deposito. Tu sei seduto su poco più di diecimila — appena l’uno per cento del milione che hai rifiutato — e cominceresti a pensare seriamente di aver scelto male. Tieni duro.

Terza decade

| Giorno | Pagamento |

|---|---|

| Giorno 21 | $10.485,76 |

| Giorno 22 | $20.971,52 |

| Giorno 23 | $41.943,04 |

| Giorno 24 | $83.886,08 |

| Giorno 25 | $167.772,16 |

| Giorno 26 | $335.544,32 |

| Giorno 27 | $671.088,64 |

| Giorno 28 | $1.342.177,28 |

| Giorno 29 | $2.684.354,56 |

| Giorno 30 | $5.368.709,12 |

Totale accumulato a fine giorno 30: $10.737.418,23. Dieci milioni, settecentotrentasette mila dollari e ventitré centesimi.

Adesso fermati. Rileggi quel numero.

Il solo trentesimo giorno — un giorno, ventiquattro ore — ti ha pagato cinque milioni e trecentosessantotto mila dollari. Più di cinque volte quello che il tuo amico ha preso all’inizio. In un giorno solo.

E il totale complessivo è quasi undici milioni.

4. Il ribaltamento

Il novantanove per cento delle persone a cui poniamo la domanda sceglie il milione. Sicure. Convinte. Sollevate, anche, per aver evitato il trabocchetto. Hanno scelto, in proporzione esatta, un decimo di quello che avrebbero potuto avere. Hanno lasciato sul tavolo $9.737.418,23.

Quasi dieci milioni. Convinte di essere state furbe.

Da questo lato — l’angolazione federativa, quella della Federation Research — quello che ci interessa non è ridere di chi sceglie male. Ci interessa capire perché la mente umana sceglie sistematicamente, ripetutamente, prevedibilmente male in questo tipo di scommessa. Perché lo stesso schema si ripeterà più avanti, su un’altra scala, con un altro asset. E vogliamo che chi legge queste righe, quando lo schema si presenterà di nuovo, lo riconosca.

Guarda la sequenza dei totali a fine decade:

Fine giorno 10 → $10,23

Fine giorno 20 → $10.485,75

Fine giorno 30 → $10.737.418,23

Ogni dieci giorni si aggiungono tre zeri al cumulato. Tre zeri puliti. Il pattern è scritto in cifre tonde, ma nei primi due terzi della scommessa è praticamente invisibile alla mente lineare. Solo nell’ultimo terzo esplode.

E c’è un dettaglio ancora più scomodo, che la Federation considera il vero cuore del paradosso. Dopo ventisei giorni — l’ottantasette per cento del tempo della scommessa, quasi tutta — sei ancora a quota $671.088,63. Il milione non l’hai ancora raggiunto. Il tuo amico ti guarda con compassione.

È al giorno ventisette che lo superi, e di poco. Dal giorno ventotto in avanti, succede una cosa che la mente lineare non riesce a vedere arrivare: negli ultimi tre giorni guadagni sette volte tutto quello che avevi accumulato nei ventisette precedenti. Il novanta per cento del tempo della scommessa produce un ottavo del risultato finale. L’ultimo dieci per cento del tempo produce i restanti sette ottavi.

E c’è una regolarità ancora più affilata, che vale la pena fissare perché torneremo a usarla. Ogni giorno che togli dalla fine, il cumulato si dimezza. Al giorno 29 hai metà. Al giorno 28 un quarto. Al giorno 27 un ottavo. Al giorno 26 un sedicesimo. Al giorno 25 un trentaduesimo. La parabola contiene tutta la sua storia compressa nell’ultimo gradino. Tutta. La storia stessa della scommessa è scritta nel suo ultimo giorno, e in nessun altro.

Quando guardiamo Bitcoin oggi e qualcuno dice “ormai è tardi, è già salito troppo”, sta dicendo una cosa che la parabola del centesimo smentisce in faccia: in una crescita geometrica, l’ultimo gradino contiene metà della partita. Il fatto che i gradini precedenti siano già stati saliti non riduce il prossimo, lo ingrandisce.

La nostra visuale federativa ritiene che questo non sia un esercizio matematico. È un teorema antropologico. Dice che la specie umana, di fronte a una crescita geometrica, non riesce a credere alla propria fortuna fino al penultimo momento utile. E quando riesce a crederci, di solito ha già scelto l’altra opzione.

Adesso che il paradosso del centesimo è chiaro, possiamo fare la cosa interessante: chiederci se esiste, nel mondo reale, un asset che si comporta esattamente così.

5. E se fosse Bitcoin?

Esiste un asset reale che si comporta come il centesimo della parabola.

Si chiama Bitcoin, e ha una sua unità minima — quella che, nel rapporto tra un Bitcoin intero e la sua frazione più piccola, occupa la stessa posizione che il centesimo occupa nel rapporto col dollaro. Si chiama satoshi, dal nome dell’inventore, e per quindici anni l’industria che lo dovrebbe spiegare ha fatto del suo meglio per non spiegarlo.

Lo ha presentato così: 0,00000935 BTC.

Oppure così: 0,000935 dollari.

Numeri con cinque, sei, sette zeri prima della prima cifra utile. Numeri che la mente umana, semplicemente, legge come niente. Non è un difetto del lettore — è il modo in cui la mente è fatta. Funziona con i numeri pieni, non con i decimali frantumati. Il numero pieno si pesa, si conta, si tasca. Lo zero virgola sparisce come un soffio.

Proviamo da soli. Fermati e fai questo esperimento — anche solo nella tua testa, ma meglio se domani lo fai davvero con qualcuno.

Chiedi a una persona qualsiasi: quanto hai in tasca in questo momento?

Risponderà, supponiamo: un dollaro. Oppure un euro. La cifra non importa.

Adesso chiedi: in che altro modo potresti chiamarlo?

Quasi sempre ti guarderà stranita. Forse risponderà con un’altra valuta — un euro è un dollaro e qualcosa, un dollaro è circa novanta centesimi di euro. Pochi, pochissimi, daranno la risposta che dal punto di vista federativo riteniamo essere quella corretta:

Cento centesimi.

Un dollaro è cento centesimi. Stessa moneta, stesso valore, due grammatiche diverse. Eppure la mente le tratta come due cose diverse: un dollaro suona come un’unità, cento centesimi suona come una piccola fortuna. Cento di qualcosa, in mano, ha sempre più peso di uno.

Adesso applichiamo la stessa logica a Bitcoin.

Oggi, con un solo dollaro, si comprano 1.070 satoshi.

Non zero virgola qualcosa. Non un decimale. Mille e settanta. Mille e settanta unità intere, contabili, accumulabili, tascabili. Lo stesso dollaro che, dall’altra parte della grammatica industriale, era 0,00000935 BTC e sembrava polvere.

Cambia tutto. Cambia il modo in cui la mente registra l’acquisto, cambia il modo in cui la mente registra il possesso, cambia il modo in cui la mente immagina la crescita futura. Da questa angolazione federativa, riteniamo che metà del fraintendimento popolare su Bitcoin sia un fraintendimento di unità di misura. Le persone non hanno rifiutato Bitcoin perché non avevano capito la tecnologia. L’hanno rifiutato perché qualcuno glielo ha mostrato in una grammatica che il cervello legge come irrilevante.

E adesso, con la grammatica corretta in mano, possiamo tornare al paradosso del centesimo.

Cosa succede se quel centesimo della scommessa non è un cent qualsiasi — è un satoshi?

Cosa succede se la parabola del raddoppio non si applica a un esperimento mentale chiuso in trenta giorni — ma a un asset vero, che esiste, che ha già attraversato una porzione della propria parabola, e che ne ha un’altra porzione ancora davanti?

Per rispondere a queste due domande dobbiamo prima fissare due cose: quanto è grande, oggi, un satoshi misurato in dollari, e a che punto della parabola ci troviamo.

Le affronteremo separatamente, nelle prossime due sezioni, prima su orizzonti diversi — tre anni e trenta anni — e poi sul lungo arco storico che parte dal 2009.

6. La parabola applicata a Bitcoin

Mettiamo da parte i dollari per un momento e ragioniamo in satoshi.

Oggi un satoshi vale, in dollari, 0,000935. Cinque zeri dopo la virgola prima di trovare una cifra utile. Lo abbiamo già visto: è il numero che il cervello rifiuta di leggere.

Ma c’è un’altra grammatica per dire la stessa cosa. Possiamo chiederci: quanto deve apprezzarsi un satoshi perché valga quanto un centesimo di dollaro? Cioè perché valga 0,01 dollari, una cifra che la mente legge come un’unità intera, un cent vero?

La risposta è: il satoshi deve fare un fattore 10,7 volte il suo valore di oggi. In altre parole, ci vogliono poco più di tre raddoppi e mezzo.

Tre raddoppi e mezzo, ricordiamolo, è quello che il paradosso del centesimo produce in tre giorni e mezzo. Per il satoshi, il cammino non si misura in giorni: si misura in cicli. E qui entrano in scena due orizzonti che la Federation considera fondamentali distinguere — uno corto, uno lungo — perché parlano a due tipi di lettori molto diversi e a due tipi di progetto di vita molto diversi.

Orizzonte A — Tre anni

Tre anni è l’arco temporale di un singolo ciclo di Bitcoin. Tra un halving e il successivo intercorrono circa quattro anni; dentro questa finestra si concentrano una fase di accumulazione, una fase di esplosione del prezzo, una fase di euforia e una fase di correzione.

Se nel prossimo ciclo — quello che ha avuto il suo halving nell’aprile 2024 e che sboccerà nei mesi successivi — il satoshi facesse tre raddoppi e mezzo, un satoshi varrebbe quanto un centesimo di dollaro. Tradotto nell’altra grammatica: un Bitcoin varrebbe un milione di dollari. Da quel momento in poi, ogni dollaro nel portafoglio del lettore comprerebbe non più 1.070 satoshi, ma 100.

Il numero degli zeri si invertirebbe. Il satoshi smetterebbe di essere “polvere” e diventerebbe la nuova unità di conto popolare. Il dollaro stesso, di fatto, verrebbe ridenominato in satoshi nella testa di chi ha già fatto il cambio di paradigma.

Questo è l’orizzonte A. Tre anni, tre raddoppi e mezzo, e la parabola del centesimo applicata a Bitcoin si chiude in pareggio col paradosso originario.

Orizzonte B — Trent’anni

Trent’anni è l’arco temporale di una vita lavorativa. È il piano d’accumulo che un ragazzo di venticinque anni, oggi, può cominciare a costruire pensando a quando ne avrà cinquantacinque. È, dall’angolazione federativa, l’orizzonte vero.

In trent’anni, secondo la cadenza del protocollo Bitcoin, avvengono circa sette halving e mezzo — sette tic del metronomo lungo, quello che ogni quattro anni dimezza la nuova offerta di Bitcoin sul mercato. Ogni halving, storicamente, ha prodotto da uno a tre raddoppi di prezzo nei due o tre anni successivi. Manteniamo qui un’ipotesi prudente: un raddoppio strutturale per ogni halving.

Sette raddoppi in trent’anni significano un fattore 128 volte il valore di partenza. Se oggi un Bitcoin vale circa 93.000 dollari, fra trent’anni — a parità di ipotesi conservativa, una sola moltiplicazione per due ogni quattro anni — varrebbe quasi dodici milioni di dollari.

Tradotto in satoshi nella tasca: oggi con un dollaro compri 1.070 sats; fra trent’anni, sempre con un dollaro, ne compreresti circa otto. Non duecento, non cinquecento. Otto satoshi. Ogni sat sarebbe quindi diventato qualcosa che vale, in proporzione, ciò che oggi è una banconota da dieci centesimi.

Adesso prendiamo il punto di vista del ragazzo di venticinque anni che oggi mette da parte cento dollari al mese in Bitcoin. Mille e duecento dollari l’anno, ai prezzi di oggi, comprano circa un milione e trecentomila satoshi all’anno. In trent’anni, quasi quaranta milioni di satoshi accumulati — cioè poco meno di mezzo Bitcoin intero.

A 0,000935 dollari per sat (prezzo di oggi), quel mezzo Bitcoin vale circa 37.000 dollari. Praticamente il capitale versato. Apparentemente, nulla di guadagnato.

Ma applicando l’ipotesi conservativa dei sette raddoppi in trent’anni — la più cauta possibile, quella che presuppone una decelerazione drastica rispetto a tutta la storia di Bitcoin fin qui — quei quasi quaranta milioni di sats valgono fra trent’anni circa quattro milioni e settecentomila dollari di oggi.

Quattro milioni e settecentomila dollari, da una somma versata di trentaseimila. Centotrenta volte il capitale investito.

E ricordiamolo: è lo scenario conservativo. Quello che presuppone che Bitcoin nei prossimi trent’anni si comporti molto, molto peggio di come si è comportato nei quindici appena passati.

Nota di trasparenza. I calcoli di questa sezione sono fatti al prezzo di Bitcoin al momento in cui questo articolo è stato scritto — circa 93.000 dollari per Bitcoin, circa 1.070 satoshi per dollaro. Il prezzo è in movimento continuo: quando il lettore leggerà queste righe sarà diverso, magari di poco, magari di molto. La logica della parabola, però, non cambia con il prezzo del giorno: cambia il punto di partenza, non la geometria del cammino.

Il salto della mente lineare

Adesso il lettore può fare due cose.

Può guardare il numero finale — quattro milioni e settecentomila — e sentire montare la stessa identica reazione di chi, davanti al paradosso del centesimo, ha risposto il milione, è ovvio. Cioè: troppo bello per essere vero, c’è una trappola da qualche parte, non ci credo.

Oppure può guardare il meccanismo che produce quel numero — sette raddoppi in trent’anni, uno ogni quattro anni, scanditi da un metronomo che è scritto nel codice del protocollo e che non ha mai saltato un battito in sedici anni — e accettare che la trappola non c’è. C’è solo, di nuovo, la matematica del raddoppio, applicata a un orizzonte temporale più lungo di quello che la mente lineare riesce a immaginare con naturalezza.

Il paradosso del centesimo dura trenta giorni e produce undici milioni. Il paradosso del satoshi dura trent’anni e — nell’ipotesi più conservativa — produce un risultato dello stesso ordine di grandezza. Stessa geometria, su una scala diversa. Stesso teorema travestito da indovinello.

Resta una sola domanda, ed è la più importante. Se la parabola del satoshi è già in moto, a che punto della parabola ci troviamo oggi?

A questa domanda è dedicata la sezione che segue. Ed è qui che la Federation deposita la sua prima Call con timestamp.

7A. Dove siamo nella parabola

Bitcoin nasce il 3 gennaio 2009, quando Satoshi Nakamoto mina il blocco numero zero — il genesis block. Per circa diciotto mesi non ha un prezzo di mercato: viene scambiato fra appassionati come una curiosità tecnica, alla pari, senza alcun riferimento monetario.

Il primo prezzo registrato risale a metà 2010: circa tre decimi di centesimo di dollaro per Bitcoin. Zero virgola zero zero tre dollari. Un Bitcoin valeva, letteralmente, meno di un decimo di centesimo. A quel prezzo, un singolo dollaro comprava circa trecentotrentamila Bitcoin interi.

Oggi, sedici anni dopo, lo stesso Bitcoin si scambia intorno ai 93.000 dollari.

Adesso facciamo l’unica operazione che conta: contiamo i raddoppi che separano quei due numeri. Da 0,003 dollari a 93.000 dollari c’è un fattore di crescita di circa trentun milioni di volte. Per coprire un fattore così grande con raddoppi successivi servono — la matematica è elementare, basta contare quante volte si moltiplica per due partendo da uno per arrivare a trentun milioni — circa venticinque raddoppi.

Venticinque.

Adesso torna mentalmente al paradosso del centesimo. Trenta raddoppi in trenta giorni, undici milioni di dollari accumulati nell’ultimo. Venticinque raddoppi era il numero che corrispondeva, sulla nostra tabella, al giorno 25 della scommessa. Vediamolo, perché è importante che il lettore lo veda con gli occhi e non solo con la testa.

A fine giorno 25 della scommessa del centesimo, hai in tasca $335.544. Più di trecentomila dollari. Una somma rispettabile. Una somma che, se ti avessero offerto trentamila dollari il primo giorno al posto del centesimo da raddoppiare, ti sarebbe sembrata impossibile.

Ma ti mancano ancora cinque giorni di scommessa. E in quei cinque giorni il cumulato passa da 335.544 dollari a 10.737.418 dollari. Trentaduemila volte tanto. In cinque giorni.

Bitcoin, oggi, è esattamente in questa posizione. Ha già percorso venticinque raddoppi di prezzo: dal primo prezzo di mercato a oggi, il valore è raddoppiato circa venticinque volte. Ma attenzione a non confondere due cose diverse, perché qui sta tutto. Una è il raddoppio di prezzo — quante volte il valore si moltiplica per due. L’altra è il tic di tempo — l’halving, il battito del protocollo che scandisce il ritmo ogni quattro anni. Sono due righelli distinti, e misurano cose distinte. Quanti raddoppi di prezzo restino davanti, nessuno può dirlo contandoli: la parabola di Bitcoin non si legge sul righello del prezzo, ma su quello del tempo. È lì — sui tic dell’halving — che dobbiamo guardare per sapere davvero a che punto siamo.